Construction Industry Scheme - CIS Guide

CONSTRUCTION INDUSTRY SCHEME - CIS

The Basics.

This article is aimed at the self-employed CIS worker. So, if you are new and just starting out as a self-employed construction worker then this article will tell you all you need to know / give you all the basic information. This information can be fragmented which means you are often reading different blogs to make sense of it all and worse still you could find conflicting information which is not helpful either.

What is the Construction Industry Scheme?

Commonly referred to simply as CIS – the construction Industry Scheme is an HMRC scheme which applies if you work as a subcontractor in the construction industry and not as an employee. So, it typically applies to self-employed individuals and the CIS rule means that the contractor is usually required to withhold a 20% or 30% tax from their payments to you. We will look at the factors that determine whether they deduct 20% or 30% before they pay you later in this article.

This is very different from other self -employed individuals not within the construction industry, who will normally receive their payments gross, that is without any tax being deducted before the payments is made to them.

It is important to the clear that even though a contractor is withholding tax under the CIS payments made to you, and you might receive documents very similar to payslips, you are not being treated as an employee and as such you will not be entitled to any of the employment rights of being one. We will look at this in more details later on in the article.

The CIS covers more than what you may typically think of as building and civil engineering work and incudes work in demolition, site clearing and cleaning, repairs and decorating, traffic management for construction purposes and installing power systems. The HMRC CIS Manual details what work is included and excluded from the CIS and definitely work a read.

Note that if you supply construction industry type services directly to a homeowner or small businesses like building repairs, then this would not fall under the CIS and the customer will pay you in full i.e. gross on receipt of your invoice.

Scope

It is important to point out that not everyone who works in the construction industry is self employed and contractors have an obligation to decide if their workers are employed or self-employed. Whilst most contractors would no doubt prefer to take on workers on a self-employed basis, self-employment is a question of fact not choice. We look at circumstances at that point to self-employment below.

5 Simple Tests that can help you determine if you are self – employed:

1. You agree to do the work, but can send someone else to do the job for you, for instance a builder can send another person with similar skills in their place, as long as the job gets done to the agreed standard and within the agreed scope. You are also are responsible for the quality of work and redoing unsatisfactory work without charging more.

2. You provide the main items of equipment or specialist tools you need to do your work, such as scaffolding, ladders and all the required materials

3. You run a business and take responsibility for it success or failure, such as finding new customers, take appointments, have your own business cards.

4. You have several customers at the same time. You can do the work how, where and when you like as along as it is agreed with the customer. For example, you can choose to work on Sundays on a building renovation work on an empty house.

5. You send an invoice for the work done to customers.

None of these tests are conclusive and must weigh different factors to get an overall picture.

If you are still unsure can seek professional advice. You could try contacting ACAS, an employment law adviser or a solicitor (many will offer a free initial consultation). You will not automatically be self -employed just because you have an existing unique taxpayer reference and complete a tax return at the end of each tax year.

There is a misconception that people who work in the construction industry are always self-employed and this is not the case. If you are in the construction industry you should work out your employment status the same way as everyone else.

Chances are if you work in the construction industry and are being treated under the construction industry scheme then you are being treated as self-employed by your engager. However, it can be difficult to spot this as under CIS you are given payments and deductions statements (PDS) which are very similar to payslips.

Registering with HMRC

Once you have established you are self employed and are working in working in the construction industry then you should consider registering under the Construction Industry Scheme (CIS).

Real Life Application: If John, a heating engineer is contracted by a local builder to run heating pipes and fit a boiler in a new build house, then his work will fall under the CIS. If he himself subcontracts out some elements of this work to a friend to help him out, then John becomes the contractor and his friend the sub contractor.

Contractors:

If you are engaging other self-employed workers to help out with various construction projects, then you are a contractor and must register with HMRC under the CIS. You can find out how to do so on Gov.uk here

Before a contractor takes on a new subcontractor they are required to “verify” them with HMRC. This is the way you check if they are registered for the Construction industry scheme – CIS or not. This verification process will tell you what rate of CIS tax you need to deduct from the subcontractor. We look at the tax deductions in a little more in the CIS Tax deductions and how they work section below.

You are required to verify every subcontractor before you pay them for the first time and to do so you will need their National Insurance and Unique Tax Reference number (UTR). The verification process is done online takes seconds to complete and the end yYou will then be issued with a CIS verification number to use when communicating with HMRC re the particular subcontractor.

Subcontractors:

As a self-employed worker, it is more likely that you will be engaged or taken on by a contractor to perform some construction work. This will mean you are a subcontractor and you can choose whether or not to register under the CIS.

GOV.UK explains how you can register for the CIS as a subcontractor and what information you will ned to be able to register. There are different methods depending on whether r not you have already registered as self employed and if you are working for yourself as a sole trader or through a different entity such as a limited company or as a partnership.

Important Note: registration under the CIS is in addition to registration as self-employed for self-assessment. This means for those new to both self-employment and the CI, there are two separate registrations. However, both can be done as the same time.

When you register for CIS you have to option to register for gross payment status. When you register for gross payment and are approved by HMRC it means that the contractor will pay you in full without deducting or withholding at tax at source. HMRC will normally approve application for gross payment status if your tax affairs are up to date.

If you do not apply for Gross payment status or are rejected by HMRC when you apply then the contractor will deduct either 20% tax from your pay or 30% if you have not registerer at all and we look at how those work below.

CIS Tax deductions and how they work.

20% CIS Tax Deductions:

If you decide to register for the CIS, then the contractor must deduct and withhold tax at a rate of 20% of the amount of your invoices. If your invoices include direct expenses such as materials bought for the job and tools hired, the tax should not be withheld from these amounts, so you should be paid 100% of these costs.

The 20% tax deduction is paid by the contractor to HMRC who treat it as an advance payment towards your income tax and National Insurance contributions (NIC) for the particular tax year, as shown by your self-assessment return.

This means you will receive 80% of the labour cost on your invoice paid directly to you, according to your agreed payment terms along with the full amounts for additional costs such as materials and tool hire.

Self - billing:

Sometimes, instead of you issuing invoices to the contractor for the work you have done and materials bought, the contractor will raise the invoice on your behalf, known as a self-billing document and send a copy to you with your payment. We have a full write up on self-billing arrangement here.

Most self-billing arrangement are set up under the VAT Regulations and typically contractors like self- billing arrangements as it means they don’t have to wait for an invoice from you.

It is important that you check the self-billing invoices you receive with your payments to make sure it is correct and if you spot and error you need to let the contractor know so they can issue the correct one. Note, you cannot issue your own correction invoice and send to the contractor.

30% CIS Tax Deduction:

If you decide not to register under the CIS then the contractor must deduct and withhold tax at a rate of 30% of the amount of your invoices for your labour. The deduction will not be taken from any materials or additional costs on your invoice.

Example of 20% and 30% CIS Tax deducted from payments.

Stellar Construction Limited, have hired a self-employed electrician, Julie and plasterer, Jonathan to work on a site where they are building fifty new houses. It is agreed that they will invoices Stellar Limited monthly, based on a ratee of £220/ day. Last month they both worked 21 days and so they each raised an invoice for £4,620.

Jonathan also bought some sand and additives at a cost of £350, so the total amount of his invoice came to £4,970 (£4,620 + £350)

Jonathan is registered for CIS but Julie just qualified as a electrician and this is her first job so she is not registered for CIS.

As she is not registered for CIS, Stellar Limited must deduct 30% from the payment to her and so she receives 70% * £4,620, £3,234. The balance of £1,386 is paid by Stellar Limited to HMRC on her behalf. This does not mean Julie’s income tax and National insurance Contributions for amount to £1,386, instead this is an advance payment towards her tax bill and will be adjusted when her tax is calculated.

As Jonathan is registered for CIS, Stellar Limited must deduct 20% of the gross labour income from the payment to him. Therefore, Jonathan receives £4,046 (£4,620*80% + £350) and the balance of £924 (£4,970 - £4,046) is paid by Stellar Limited to HMRC on his behalf.

Self-Assessment Tax Returns

You will usually need to complete a self-assessment tax return and will include your gross self-employment income on the return. This is your total sales income, which will be the amount you have invoiced, not the amount you received after the CIS deductions. This means that even if your invoice includes amounts for things like materials, tool hire etc. Your tax return must also include any business expenses that are to be deducted from your self-employed income to arrive at your self-employed profit.

The amount of tax that has been deducted under the CIS from your payments would be entered in box 38 on page SES32 of the self-employment (short) pages and box 81 on page SEF4 of the self-employment (full) pages. This will mean that when your tax and NIC are calculated the advance payments that have been made through CIS deductions will be taken into account.

Let’s use an example to show how this works.

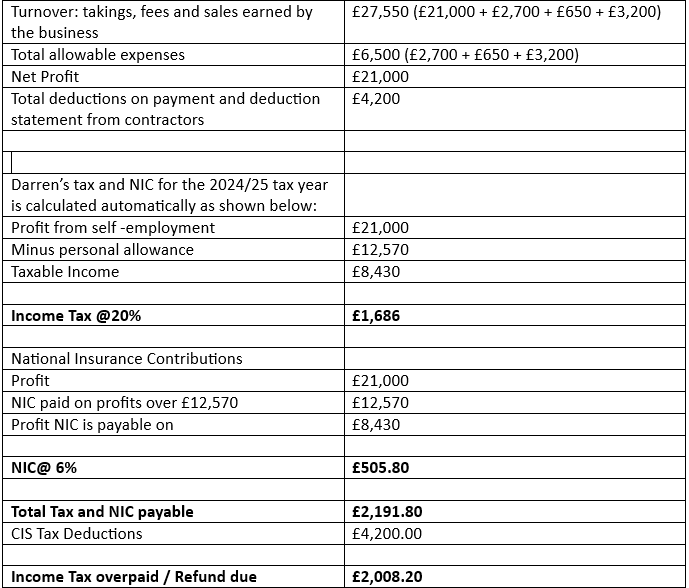

Darren is a self-employed builder, who is CIS registered but not using the gross payment scheme. He has no other taxable income in the year.

He prepares accounts for he tax return using HMRC’s recommended Cash Basis. During the 2024/25, he invoiced, and was paid Labour costs of £21,000. He also invoiced out the expenses below all of which he was paid for

1 ) Materials : £2,700

2 ) Tool Hire: £650

3 )Other allowable business expenses : £3,200

He always sure to receive monthly Payment and Deduction statement for every contractor he works for. These statements show what she had been paid and what CIS deductions have been withheld from him. He has 20% CIS deductions (so £21,000 * 20% = £4,200) in the year but has been paid in full for all the other costs he invoiced.

As can be seen Darren is due a refund of £2,008.20.

Darren’s tax position (of overpaying tax through the CIS deduction and being due a refund) is common to may self employed sole traders who are registered for the CIS but who do not have gross payment status.

The refund usually arises because CIS deductions are based on sales income and therefore do not take account of the tax-free personal allowance or business expenses.

CIS Pay and Deduction Statements

Contractors are required to provide at least one payment and deduction statement each tax month and withing 14 days of the end of the tax month to the each subcontractor they have deducted CIS tax from.

This statement must show the contractors name, details of the payments made to the subcontractor, cost of any materials incurred and the deductions made from the payments. If you have lost or are missing statements, then you need to approach the contractors and ask for copies. They have a legal obligation to provide them to you.

It is very important that you retain these statements and details of all business expenses as you will need them to complete your tax return.

The contractor should be reporting and paying over all CIS tax withheld from you to HMRC. This means HMRC should have a copy of your pay and tax details. HMRC will only provide you with the information from their own systems where you can show that you have genuine need and that you have made every effort to obtain a copy from the contractor. To obtain a copy you need to write to.

PT Operations North East England

HM Revenue and Customs

BX9 1BX

Construction Industry Scheme and Limited Companies.

It is possible to supply your services through your own Limited company, which is very different from being self-employed.

Generally, providing your services through a Limited Company may not a suitable way to trade for the lower profit-making business. Especially if it Is a simple one-man band business with no employees. This is because of all the administrative considerations such as filing annual confirmation statements and accounts to Companies House, Annual accounts and corporation tax to HMRC, the need to run a payroll, in addition to then completing a self-assessment tax return as a company director.

If you do trade as a Limited Company, then you should be aware that the CIS applies to companies as well as to individuals. Where CIS tax has been withheld at source from payments made to a company, then the deductions made may be set against the company’s other liabilities such as PAYE and corporation tax.

If this is an avenue you would like to explore especially if your sole trader business is now making more profit and you are or thinking of taking on subcontractors to work for you, then you should consider obtaining professional assistance.

VAT and CIS Deductions .

If you are VAT registered, then CIS deductions are not withheld on the VAT element of your invoice.

VAT is a complex tax – any benefits there are of entering the VAT regime can be reduced or wiped out by additional administration, professional accountancy fees or penalties for getting things wrong. Voluntarily entering the VAT regime is therefore not something to be undertaken lightly.

In addition, on 1st March 2021, a domestic reverse charge was introduced aimed at tackling fraud in the construction sector. The VAT reverse charges rules will apply to suppliers of specified services, reported under the CIS.

You can watch a HMRC webinar on GOV.UK on these reverse charge rules

Example

Andrew is a VAT registered self-employed builder and he is a subcontractor under CIS for Stellar Limited. He has sent an invoice to Stellar Limited for £39,000, which is made up of the following amounts:

Labour: £25,000

Material: £7,500

VAT : £6,500

Stellar Limited must deduct CIS tax at 20% on his labour charge of £5,000 (£25,000*20%). Therefore, Andrew will receive £34,000 (£25,000 - £5,000 + £7,500 + £6,500)

Construction Industry Scheme Tax Refunds:

We have seen that if you are registered under the CIS scheme, contractors are required to deduct 20% from their payments to you and 30% if you are not registered and work as a subcontractor. If you are self employed and on low income, a refund will normally arise because of the expenses of trade and because you will normally have the personal allowance for the tax year available. All of which are not taken into account when the deductions are taken from your payment.

You may be able to claim tax relief in your self-assessment tax return for any expenses that you incurred wholly and exclusively in relation to your work. Some of these allowable expenses include:

Costs of goods bought for resale or goods used. For example, building materials like sand, cement, wood, roofing materials etc

Wages and salaries (if you have employees that help you in the business ) or payments made to other subcontractors

Car, van and travel expenses

Rent, rates, power and insurance costs

Phone, stationery and other office costs

Advertising and marketing

Interest on loans

Bad debts written off

Accountancy, legal and other professional fees

Other business expenses incurred wholly and exclusively because of the business

It is worth bearing in mind, because in the event of a compliance check into your self-assessment tax return, you may be asked by HMRC to provide evidence that you incurred the expenses and that it was wholly and exclusively for the business. So, it is important that you keep good business records such as receipts of all expenses.

It is not a good idea to make these business expenses up or put in private ones, so as to get a bigger refund. It is illegal to do so and the penalties are severe.

How to Claim Your CIS Tax refund:

We have established that if you are self-employed and work under the CIS, you will need to file a self-assessment tax return and your refund will be generated as part of this process.

Completing and submitting a self-assessment tax return can be daunting especially if this is your first time or first year in business. You can choose to have a go at doing it yourself, there is a lot of information on line but you can also use a tax agent or an accountant to help you. The choice is entirely yours. My recommendation would be to get professional help especially if it is your first year and as you become more familiar with the process can decide to have a go at doing it yourself.

It is worth bearing in mind that there are penalties associated with incorrect tax return, so worth thinking carefully about whether to have a go at doing it yourself or getting professional help.

Blog content is for information purposes only and over time may become outdated as the tax landscape is constantly changing, although we do strive to keep it current and up to date. It is written to help you understand your taxes and is not to be relied upon as professional accounting, tax and legal advice. For additional help please contact our team, or a professional adviser.

Bookkeeping

Email:

Contact Us

support@rhodiumaccounting.co.uk

© 2026. All rights reserved | Privacy Policy | Terms and Conditions

Monthly Management Reporting

Budgets & Forecasts

Cash flow Optimisation

Processes and Controls