How To Calculate Your Self Employed Business Profits.

SOLE TRADERS

This article is aimed at new sole traders starting business on or after the 6th April 2024 as it only looks at the new HMRC rules from that date. At the end you should feel confident that you have the basics of how to put together your first set of accounts.

It is aimed at businesses who provide services like hairdressers, electricians, carers etc and does not cater for the list of businesses at the bottom of the page as they are more complex and different rules apply to them.

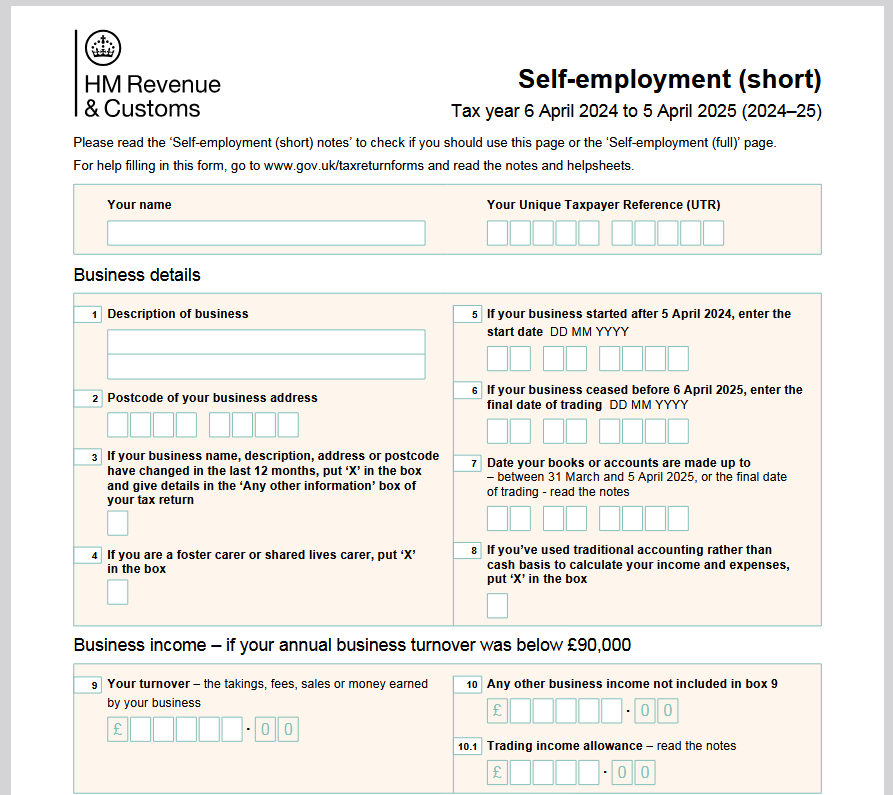

I have also included screen shots from the Supplementary Pages SA103S (used to record self -employment income and expenses ) on the SA100 Self – Self Assessment Tax Return form which will hopefully help you visualise how it all comes together.

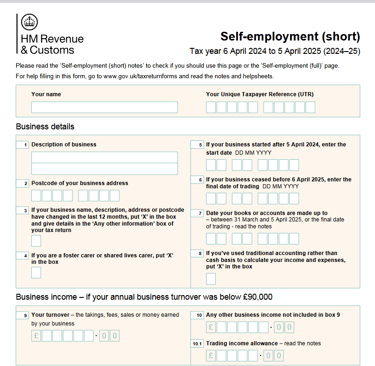

ND: The S on the SA103S stands for short and this form is to be used if your business income is less than £90,000 in the accounting period. If your business income is more than £90,000 then you will need to use the long form.

Lets start by looking at the time frame / the period for preparing a set of business accounts

Accounting Period

Your first accounting period starts from the day you commence your business and will usually be a 12-month period (but can sometimes be longer or shorter). Your business transactions such as income and expenses that fall within this period will go towards calculating the overall profit or loss for the business for the year – see boxes 5 & 7 of S103S of the supplementary pages of the self-assessment tax return.

Choosing an Accounting End date:

In the past you could choose any month as the end date of your accounting period. So as an example, lets assume you started your sole trader business on the 15th of May 2024, you could decide to end your first accounting period on the 31st of December 2024 (less than 12 months ) and then use 1st of January 2025 to 31st December 2025 as your second accounting period and so on. So, you could choose whatever date you liked or you thought would suit your business.

In April 2024, HMRC introduced the basis period reform which effectively encourages new sole traders to use an accounting period that is very similar to the tax year. So going back to our previous example instead of ending your first accounting period on the 31st of December 2024, it would be preferable to let it run to the 31st March 2025. Doing so will mean your second accounting period will run from 1st April 2025 to 31st March 2026 and every 12 months thereafter.

You can also make your accounting period the same as the tax year ending on the 5th of April but businesses use 31st of March as it ties up neatly to the end of a calendar month and HMRC treats an accounting period ending on the 31st of March as ending on the 5th of April of the same year.

In summary if you are starting your business after 6th April 2024, it may be easier and simpler to tie it with the tax year unless your business would greatly benefit from using another period which you can discuss with a professional.

Accounting Basis.

There are two ways you use to prepare your business accounts: see box 8 of SA103S.

a) the cash basis or

b) the accruals basis.

The cash basis is the simpler of the two methods and from 2024/25 tax year HMRC is encouraging more businesses to use it and will be the default (assumed ) method. So HMRC will assume you are using this method unless you specifically tell them otherwise by electing (choosing) the accruals basis. And you elect accruals (sometimes called the traditional basis of accounting) by ticking a box on your self-assessment tax return. Your self-assessment tax return contains your

What is the Cash Basis?

The cash basis of accounting means accounting for income and expenditure when payment is received or made. So, you use your cash in and out in your accounting period to calculate the profit or loss for the period.

It is the easier and simpler of the two methods and if you are just starting out in business as a sole trader then it is easier to follow HMRC’s nudge and use the Cash basis unless you are absolutely certain the accrual basis works better for your business, in which case you make an election to use that method.

If you have been in business for some time as a sole trader and was using the accruals basis and wish to change to the cash basis, you will need to make accounting and tax adjustments that arise from the transition. This can be a complex undertaking, because of the rules on how it should be done, so if you wish to change to the cash basis you should speak to an accountant.

In the year to 31st March 2025, Belle made a profit of £14,357.51. This is the amount she is going to get taxed on.

Total Income

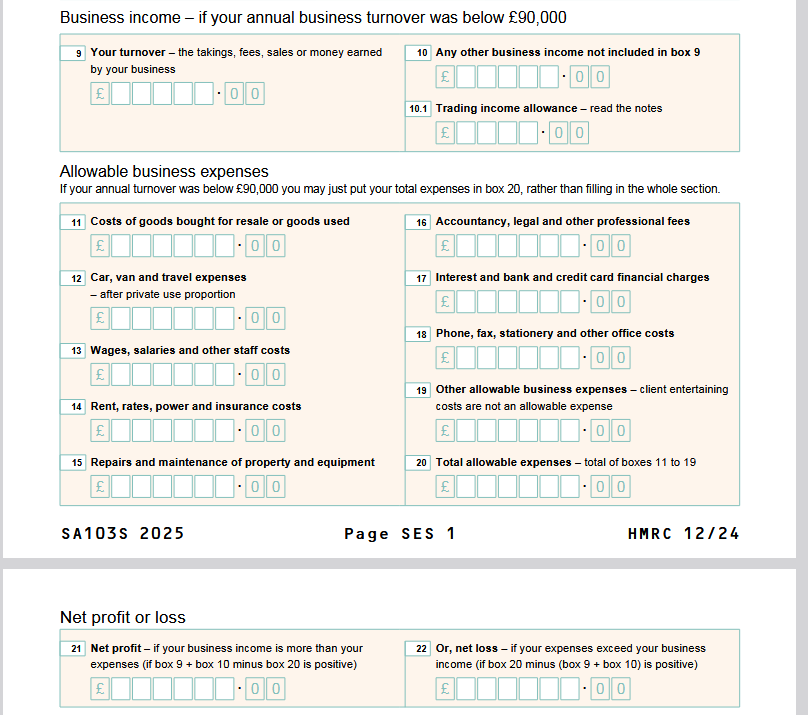

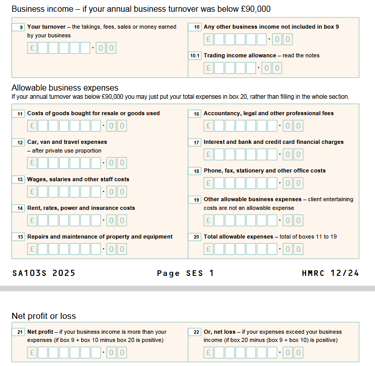

Also known as your gross income, is all your business income in the accounting period. It is also sometimes called turnover or sales. See boxes 9&10

This information should form part of your day-to-day business records and should be fairly easy to calculate.

It is worth pointing out that if you earn any income through an online platform and you use a payment facility such as GoCardless, it is likely there will be fees deducted before you received the income payment. In these circumstances, your gross income is the total income before any expense deductions by the platform

Tips:

Tipping is common in many lines of self-employed work and your total income should include any cash-in-hand-payments or tips.

So, if you are a self-employed trades person, beautician etc it is important to include all tips you receive when working out your self-employed income for your tax return and this includes tips from cash, cards or electronic apps.

Business Expenses:

Relatively self-explanatory, a business expense is a cost you have incurred or money you have spent in order to run your business or make a sale. So, if you are in the service business such as being a carer you may have to travel to clients have to buy a bus pass or buy Personal protective equipment (PPE).

What is important to note is that not all the expenses you incur as part of running your business will be tax deductible. For example, costs of entertaining clients, cost of ordinary clothing, payments you make to yourself also known as drawings. The screen shot below shows boxes 11 – 20 on the supplementary form to give an idea of the allowable business expenses.

HM Revenue and Customs Helpsheet HS222 contains a useful table of the most common allowable and disallowable expenses and is worth having a glance through.

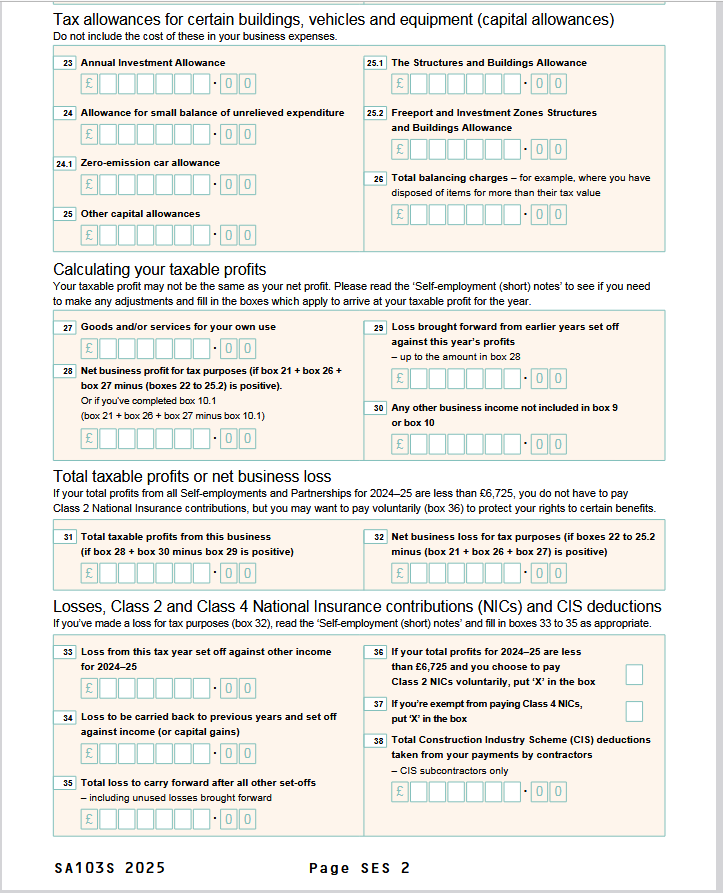

Not all the business costs or expense you incur will the tax man (HMRC ) allow as a normal business deductible expense, especially high-ticket items like cars, vans, machines, equipment etc. If these items are bought purely for business use, then HMRC grants what is called Capital Allowances.

Capital allowances are a type of tax relief for businesses. They let you deduct some or all of the value of an item from your profits before you pay tax. See boxes 23 – 31 of the supplementary form that shows the capital allowances.

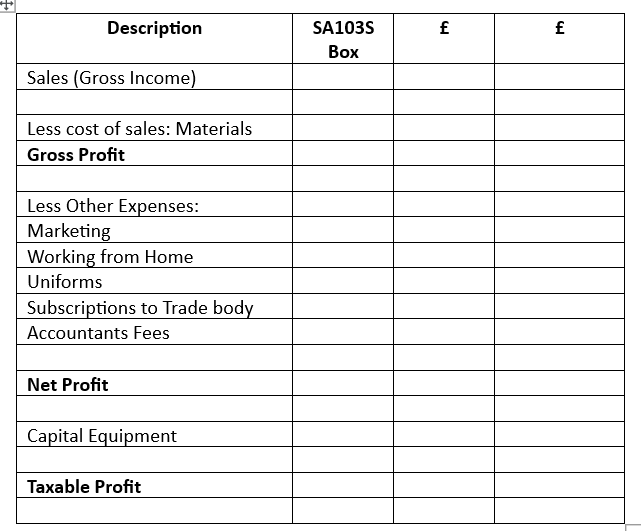

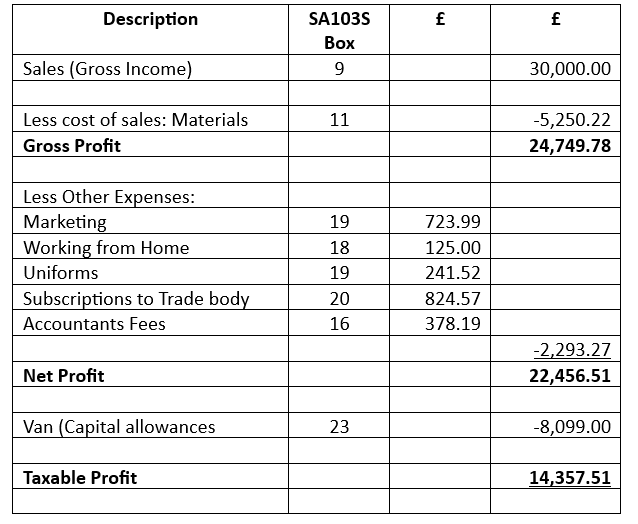

Below is an illustration of a set of accounts using the template and the dates from our previous examples.

Belle, a self-employed electrician started business on the 15th May 2024 and decides to use 31st March 2025 as her accounting end date. So, her first accounting period is 15th May 2024 – 31st March 2025 (10.5 months)

All her business income and expenses in that period are as shown below.

In the year to 31st March 2025, Belle made a profit of £14,357.51. This is the amount she is going to get taxed on.

If you would like a ready-made profit and loss template, that will save you time and energy and all you have to do is add your numbers, you can get it here.

You cannot use the cash basis if your business is in any of the ones listed below:

Lloyd’s underwriters

farming businesses with a current herd basis election

farming and creative businesses with a section 221 ITTOIA profit averaging election

businesses that have claimed business premises renovation allowance

businesses that carry on a mineral extraction trade

businesses that have claimed research and development allowance

dealers in securities

relief for mineral royalties

lease premiums

ministers of religion

pool betting duty

intermediaries treated as making employment payments

managed service companies

waste disposal

cemeteries and crematoria

Now that we have looked at income, expenses and capital allowances are, let's look at how everything comes together to prepare a set of accoutns to arrive at your taxable profits.

Below is a simple format of how you an set up your business records on monthly basis so you have an idea of how your business is performing.

Bookkeeping

Email:

Contact Us

support@rhodiumaccounting.co.uk

© 2026. All rights reserved | Privacy Policy | Terms and Conditions

Monthly Management Reporting

Budgets & Forecasts

Cash flow Optimisation

Processes and Controls