National Insurance Numbers, Contributions and State Benefit Entitlement.

NATIONAL INSURANCE

Did you know it is possible to overpay National Insurance?

In this article we will look at National Insurance, what are they, why you pay them, how you make National Insurance Contributions and how to check your National Insurance records, whether you are employed, self -employed, in a partnership or not even working but claiming some state benefits.

What is a National Insurance Number?

If you want to work or claim benefits in the UK, you must have a National Insurance number.

Also sometimes called a NINO, a National Insurance number is a unique number used to identity individuals above the age of 16 and resident in the UK. It is made up of 2 letters, 6 numbers and a final letter at the end. So it would normally read something like this PB 14 56 78 A.

Although it is unique to you, it is not a form of identification and you must never use someone else’s National Insurance Number nor you should not allow anyone to use your National Insurance number.

How is Your National Insurance Number and National Insurance Contributions Linked?

Your National Insurance number (NINO) and National Insurance Contributions are intrinsically linked. As explained earlier, your NINO is a unique identifier and it is used to track your National Insurance contributions and ensure they are correctly recorded against your name. So essentially, your National Insurance Number is like an account number for your National Insurance record. Each time you pay National insurance, your contributions and other taxes are recorded against your NINO with the HMRC.

Why make National Insurance Contributions and What are they?

National Insurance contributions are essentially a tax on your earnings and the purpose of National Insurance Contributions is to fund and contribute to various social security benefits and the NHS. Specifically, it helps pay for the state pension, the NHS, unemployment benefits, sickness and disability allowance and is used to determine your eligibility for certain state benefits such as state pension. So, your entitlement to some UK state benefits depends on sufficient NIC’s being paid (or treated as paid, or credited) in a qualifying year.

You pay National Insurance contributions (NIC) if you are:

Employed or self employed.

Aged 16 and over but below the state pension age.

The amount of NICs you pay depends on how much you earn, and are only payable on earnings from working, not on investment income, such as bank interest and dividends, pension or rental income.

The way in which you work will affect the type (class) of NIC’s you pay and you usually stop paying NIC’s when you reach state pension age, even if you continue to work. The exception is class 4 NIC for the self-employed, which you pay for the whole tax year in which you reach state pension age, and then stop thereafter.

The 4 Classes of NIC’s paid by Self Employed and Employeed Individuals.

Class 1 NICs: You pay class 1 NIC’s if you are an employee, earn above a certain amount, through the PAYE (Pay As You Earn) system. You employer deducts class I NIC’s from your gross wages before deductions, together with any income tax due, and pays you the net amount after deductions. Your employers also pay class 1 national insurance contributions on your earnings.

Class 2 NICs: Class 2 NICs are usually relevant for people who are self-employed, in addition to class 4 NIC’s and can count towards entitlement to certain contributory state benefits.

The rules around paying class 2 NICs changed in the April 2024, so 2024/25 tax year. Class 2 NICs are no longer required to be paid by self-employed individuals with profits of over £6,725 from the 2024/25 tax year, but they will be treated as having paid them.

However if you are self-employed and your business profits are below £6,725 for the 2024/25 tax year, it is possible to pay voluntary class 2 NICs (since you will not be treated as having paid them ) to preserve your entitlement to certain state benefits. This small profits threshold increased to £6,845 in the 2025/26 tax year.

Class 3 NICs: These are voluntary and count towards your state pension entitlement only. You can pay class 3 NIC’s if you want to protect your future entitlement to state pension; they do not gain you entitlement to any other contributory state benefits.

Class 3 NIC’s are more expensive than voluntary class 2 contributions and so it is worth considering if you are entitled to pay class 2 NIC’s before paying class 3.

Class 3 National Insurance are £17.45 per week compared to £3.45 per week for Class 2. You can pay for class 3 NIC’s via monthly Direct debit, or through lump sum payments.

Class 4 NICs: You pay these if you are self employed and your profits are above a certain threshold. These do not count towards any state benefits and are paid through self-assessment. You can read more on how class 4 NICs are calculated in our article: Self Employed National Insurance: What You Need to Know

I have seen some conflicting information online regarding class 2 NIC’s and I just want to clarify that as from April 2024, self- employed individuals with profits of over £6,725 are no longer required to pay class 2 Nationals Insurance but they will be treated as having paid them so their entitlement to state benefits as a result of paying class 2 NICs is preserved.

National Insurance Credits: If you are unable to work or have limited ability to work, you might be entitled to National Insurance credits. Sometimes these are given automatically but you may need to claim them at other times.

It is important to remebre that Class 4 NIC’s do not count towards any state benefits.

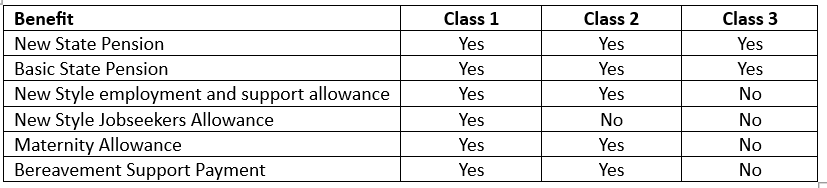

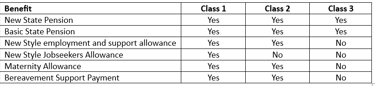

Below is a table that shows the various classes of NIC and the state benefits they entitle you to:

It is worth noting that there are exceptions to the above such as volunteer development workes and there are other benefits, which provided the rules for claiming apply to you, it does not matter whether you have paid any or enough NIC.

Listed below are some state benefits that don’t depend on National Insurance Contributions.

Universal Credit

Child benefit

Carer’s allowance

Attendance allowance and disability living allowance

Personal independent allowance

Severe disablement allowance

War widow's or widower's pension

Pension credit

How to Access and Check your NIC record to Ensure they are correct:

HMRC keep a record of the NIC’s individuals pay (or are treated as having paid) and the National Insurance credits they have received. It is important that you check your National Insurance records so you know what you have contributed and where the gaps are, if any. Filling any gaps and correcting any errors identified will ensure you are entitled to and get the maximum state benefits as a result of making those contributions.

You can check your National Insurance records by:

Logging into your personal tax account with HMRC. If you don’t have one already you can set one up following this link – HMRC personal tax account set up.

Downloading and logging into HMRC App. This is another very good way to get access to all your real time tax information with HMRC

Applying online using this form: A slower method but nonetheless an option.

Calling the HMRC National Insurance Help line details here or writing to HMRC using the details here.

The last two options are perhaps the slowest. I would highly recommend setting up an HMRC account or getting the app or even having both so you always have your most up to date information about you tax and National insurance records to hand.

Refunds of Overpaid or Incorrectly Paid National Insurance Contributions

There is a limit to the amount of NIC’s you need to pay in a tax year and this is across all the different classes of contribution.

If you have had only one employment, it is highly unlikely that you would have overpaid NICs but it is possible to have overpaid NICs in the four circumstances listed below:

You were employed and self employed at the same time and paid both class 1 and class 4 NIC’s.

You had more than one employment at the same time in a tax year and paid class 1 NICs on both.

You paid class 4 NICs on profits from self-employment in respect of a tax year after you reached state pension age.

You carried one working after state pension age and your employer continued to deduct class 1 NIC’s

Unlike tax, HMRC do not generally reconcile each individual’s National Insurance Contributions. This is because it is relatively uncommon for an individual to have paid the wrong amount of NIC’s.

If you overpay NIC’s or pay NIC’s incorrectly you can claim a refund. Just follow this link to do so https://www.gov.uk/claim-national-insurance-refund

And if you are still working at two or more jobs in a tax year, then you can apply to HMRC for a deferment of Class 1 National Insurance Contributions so that the upper rate only 2% is applied on the second job to avoid overpaying NIC. You can apply for the deferment online or by post by following this link and at the end of the tav year HMRC will issue a direct assessment is any further NIC is due.

Still have questions? You can contact us here and we would be more than happy to help.

Blog content is for information purposes only and over time may become outdated as the tax landscape is constantly changing, although we do strive to keep it current and up to date. It is written to help you understand your taxes and is not to be relied upon as professional accounting, tax and legal advice. For additional help please contact our team, or a professional adviser.

Bookkeeping

Email:

Contact Us

support@rhodiumaccounting.co.uk

© 2026. All rights reserved | Privacy Policy | Terms and Conditions

Monthly Management Reporting

Budgets & Forecasts

Cash flow Optimisation

Processes and Controls