Simplified Expenses for the Self-Employed Carer

SOLE TRADERS

There are three types of expenses where you can claim a flat rate allowance for the expense rather than the actual cost or an apportionment of the total cost (when there is both business and private usage)

These flat rate allowances are called simplified expenses and are designed to make life easier for the self -employed or those in partnerships to keep business records and prepare their tax returns.

It is important to bear in mind that it may not always be preferable to claim the simplified expenses as you may be able to claim a greater amount by using the actual cost, although it may be more complicated and / or time-consuming to calculate the actual business expense.

The Three Types of simplified expenses are for:

Working from home.

You have to work more than 25hours in a month (time that can be included, speaking to your clients, looking for new clients (marketing your services), doing your accounts and completing your tax return before you can claim the flat rate allowance to cover household expenses. The rates for the 2024/25 tax year and the 2025/26 are the same and are shown below:

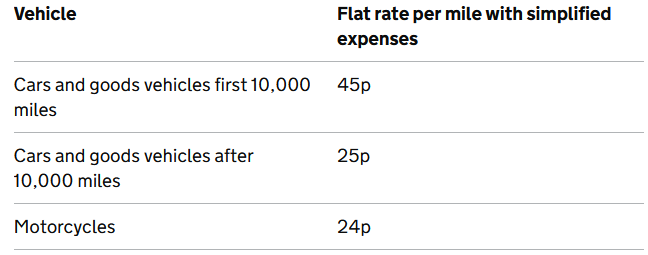

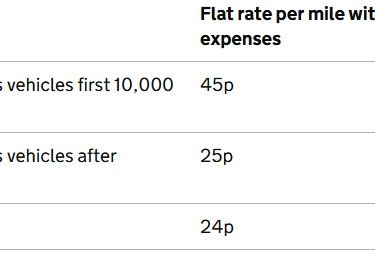

25 to 50 hours/month - £10/month

51 to 100 hours/month - £18/month

101 or more hours/month - £26/month

So the maximum you can claim using simplified expenses for working from home is £26 * 12months = £312.

This claim is instead of actual expenses like a proportion of utilities. In addition to this you can still claim a business proportion of household expenses for example council tax, internet and mortgage interest.

These flat rate allowances are relatively modest amounts and may result in a smaller claim than if you claim an appropriate proportion of your actual costs.

Vehicle Expenses

You can use simplified expenses for your car if you drive from client to client during your shift. It can also be applied to motorcycles and vans (although it is highly unlikely that you will be using a van if you are a carer.

You do not have to use flat rate for all your vehicles but once you have chosen this route then you have to stick to it for as long as you use that vehicle in your business. Basically, you cannot chop and change between accounting periods.

If you chose to use the simplified expenses method then you will need to keep a record of the number of miles you travel for business. You will still be able to claim other travel expenses such as train and bus journeys, car parking etc.

If you have already claim Capital Allowances for a vehicle you cannot use the simplified expenses approach.

In other words, once you decide you want to use the simplified expenses approach for vehicle expenses you then you cannot claim any other vehicle related costs such as insurance servicing and repairs and capital allowances on the cost of the car. The same applies if you have already claimed capital allowance on the car, you cannot then in later years claim simplified expenses for that particular car.

It is recommended that for the first year of any new vehicle or a new business, you keep track of both your business mileage and your actual motor expenses to work out which method to use.

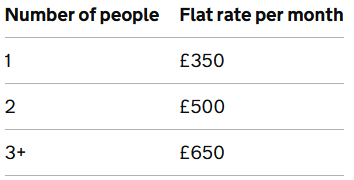

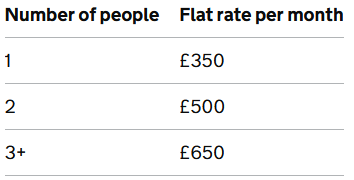

Living at Your Business Premises

The third simplified expenses is living at your business premises which will be applicable if you are self-employed, run your own care home and also live in it.

You can use simplified expenses instead of working out the split between what you spend for your private and business use of the premises.

You need to calculate the total expenses for the premises and then use the flat rate to calculate what is not deductible and amount that is left is what you will be able to deduct as an allowable expense.

Let us use an example

You run a small care home and live in it the for the entire year. Let's also assume your overall business expenses in the year was £35,000.

Flat rate: 12 months * £350 per month = £4,200 (this is the amount you will not be able to claim)

Your allowable business expense will there be £30,800 (£35,000 - £4,200)

If another member of the family lives at the premises for part of the year, you will need to factor them into the calculation for the period they live within the property.

Let’s use another example:

You live in the property for the whole year and your son who is at university comes home and lives with you for 4 months of the year.

Calculation:

Flat rate for you : 1 person 8 months = £350 * 8 = £2,800

Flat Rate for 2 of you : 2 people 4 months = £500 * 4 = £2,000

Total that is disallowed = £4,800 and the amount you can claim as business expense = £30,200 (£35,000 - £2,000 - £2,800)

If you are new to self employment and would like to understand the “actual method” for claiming business expenses, our Self Employment Guide has all the information you need. It will give you enough information to help you decide which approach is best for your business helping you to save tax.

Making Tax digital is just round the corner and if you think your gross income from 6th April 2024 - 5th April 2025 is going to be above £50,000 then you will be required to start filing quarterly returns from April 2026. You can read all about Making Tax Digital for Income Tax in our blog post here

Bookkeeping

Email:

Contact Us

support@rhodiumaccounting.co.uk

© 2026. All rights reserved | Privacy Policy | Terms and Conditions

Monthly Management Reporting

Budgets & Forecasts

Cash flow Optimisation

Processes and Controls