Workplace Pension Contributions - How to claim your Money Back.

PENSIONS

Putting money into your pension is one of the most tax-efficient things you can do as a UK tax payer. But if you are earning more than £50,270 and therefore in the 40% higher tax bracket, there is a good chance you are not getting all the tax relief you are entitled to. In fact, higher earners in the UK miss out on hundreds of millions in unclaimed pension tax relief every year.

This article will walk you through how pension tax relief works in the UK, who can claim extra and how to do it, whether you are employed or self-employed.

What is the Pension Tax Relief?

When you pay into a pension, the government gives you back the income tax you paid on that money in the form of tax relief. It is their way of encouraging you to save for retirement.

If you are a basic rate tax payer i.e. your annual earning is less than £50,270, your pension provider will automatically claim this back for you so you don’t have to do anything. For example,

You pay £200 into your pension,

The government will add £50,

You end up with £250 in your pension pot.

That is an increase of 25% on the £200 you paid in and you did not have to do anything.

But if you earn more than £50,270 in a tax year and therefore fall into the higher or additional rate tax bracket, you are entitled to even more tax relief but you have to claim it yourself as this is not automatically done for you. This is where most lose out as most people are not aware of this additional relief let alone how to claim it back. But that will not be you after reading this article.

What is Higher and Additional Rate Pension Tax Relief?

If you pay income tax at 40% or 45% ( or 42% and 47% in Scotland) you could be missing out on hundreds or thousands in unclaimed pension tax relief, unless you claim it.

Tax relief on pension works by giving you back the tax you paid on the money you put away for your retirement. The higher your tax rate, the more you can claim.

40% Higher rate tax payers can claim up to 40% total tax relief on their pension contributions. For example, if you contribute £6,054 into your pension pot and the tax man tops it up with 40% tax relief, you could end up with £10,000.

45% Additional rate tax payers can claim up to 45% total tax relief on their pension contributions. This means £10,000 of pensions contributions could cost as little as £5,500.

The issue? Only 20% is added automatically. The rest? That is for you to claim or lose.

Are you Eligible to claim?

Yes, you can claim tax relief on your personal contributions to a registered pension scheme if you paid them before you reach the age of 75 and have:

been a UK resident in the tax year

had taxable UK earnings, such as income from employment or profits from self-employment

had UK taxable earnings from overseas Crown employment (or your spouse or civil partner did)

been a UK resident when you joined the scheme and at any time in the 4 tax years before the tax year you are claiming for. So, for example, if you are claiming for the 2025/26, you can claim back to 2021/22

if you are a higher rate or additional tax payer and your workplace pension (if you are employee )is set up in such a way that your pension contributions are taken after tax.

If you are not sure if you are receiving tax relief, check with your employer or pension provider which contribution arrangement your workplace pensions use. You need to know whether it is net pay, relief at source or salary sacrifice. Most pension providers will automatically claim the basic rate pension relief back but it is worth double checking to be sure that is indeed happening. In short you need to ask and understand the type of workplace pension you have been enrolled in.

How much could I get back?

The general rule of thumb is that you can claim extra relief on pension contributions up to the amount of income you pay higher or additional rate of tax on. On the other hand, if your pension contribution is more than the amount you earn above the higher rate band, only part of your contribution will be eligible for the higher rate tax relief.

Let’s look at two different examples which will hopefully help to clarify how the pension tax relief works.

Pension Tax Relief - All Pension contributions from higher rate tax bracket.

Harriett earns £60,000 and wants to end up with £6,000 in her pension at the end of the tax year. The £6,000 is also what is known as her gross pension contributions. Because of the way her workplace pension has been set up she is making the contributions after tax and national insurance deductions.

Below is how she will be eligible for pension tax relief.

a) She will automatically get 25% added to the pot by the tax man as the basic pension tax relief. So, to get the £6,000 she will need to contribute £4,800 in pension contributions and the tax man will add 20% at £6,000 = £1,200.

b) She will then need to claim the additional pension tax relief as a higher rate tax payer on £9,730 (earnings between £60,000 and £50,270, taxed at 40%) as cash back. This is another £1,200 (20% * £6,000) that she will get back.

So over all it will cost her £3,600 to get a pension pot of £6,000.

It is worth noting here that the total £6,000 gross pension contribution fell into higher rate tax bracket, so she is able to claim, higher rate pension relief on all the £6,000

Pension Tax Relief – Pension contributions from basic and higher rate tax brackets

Using Harriett again but this time let us assume she earns £54,000 and wants to end up with the same £6,000 in gross pension contributions at the end of the tax year

a) Very similar to the first example, she will automatically get 25% added to the pot by the tax man as the basic pension tax relief. So, to get the £6,000 she will need to contribute £4,800 in pension contributions and the tax man will add 20% at £6,000 = £1,200.

b) She will then need to claim the additional pension tax relief as a higher rate tax payer on £3,730 (her earnings between £54,000 and £50,270, taxed at 40%). This comes to £746.

This means for Harriette in the second scenario, it will cost her £4,054 to get a gross pension pot of £6,000. Notice that she is contributing more in this second scenario compared to the first because not all of her pension contributions are coming from 40% tax bracket.

How to claim the Higher or Additional rate relief.

You can now claim the additional tax relief 2 different ways

· Via self-assessment tax return

· New HMRC’s online Claim Tool

Self-Assessment : If you complete self-assessment tax returns, you must claim through your tax return (for the current year and any previous years). Use this service if you are claiming a tax relief through your tax code for just the current year.

On your self-assessment tax return, go to the tax reliefs section and enter your total gross pension contributions (i.e. the amount you paid and the basic relief claimed. You should be able to get a statement from your pension provider, confirming the total amount)

Using our Harriette example, she will enter her contributions of £4,800 and the basic rate pension relief claimed by her provider £1,200, a total of £6,000. She will enter this amount in both cases and HMRC will refund i.e. give her cash refund of £1,200 or £746. She could also opt to have this back in her tax code if she is an employee.

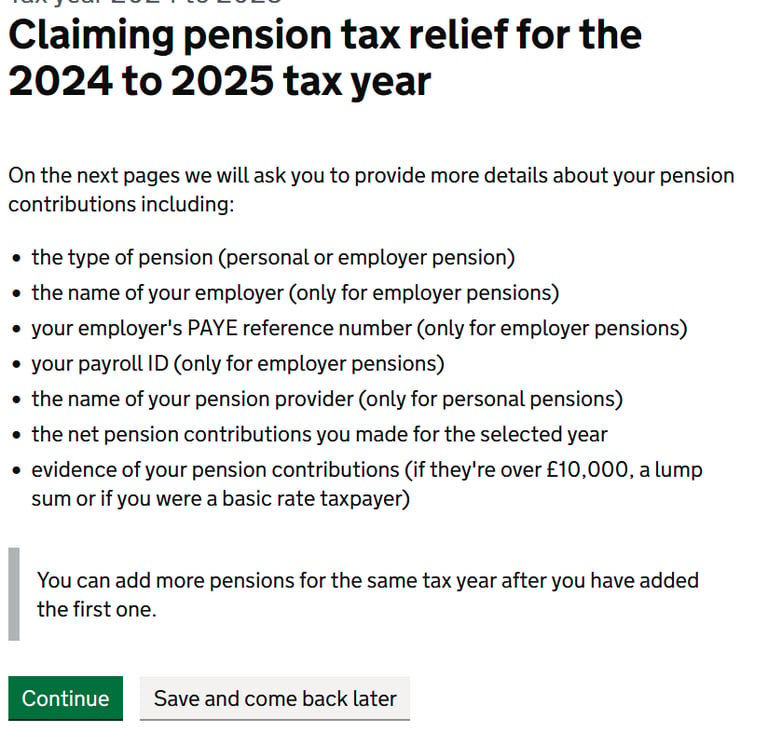

New HMRC Online Claim Tool: There is now a faster option for those who don’t file a tax return. Higher and additional rate tax payers can now claim tax relief via HMRC Online Pension Tax Relief Tool . To claim you will need the information below to hand.

Your National Insurance Number.

Details of the pension such as the pension type, the provider, the net amount of pension contributions for each tax year you want to claim for, proof of payment from your pension provider and your payroll or reference number.

And of course, You will need a Government Gateway Account to be able to use this tool. I will recommend having a Government gateway account anyway (even if you don’t need it for pension claim ) so you can see and manage your tax records with HMRC. It is also far quicker and easier to get your tax information without having to call the HMRC.

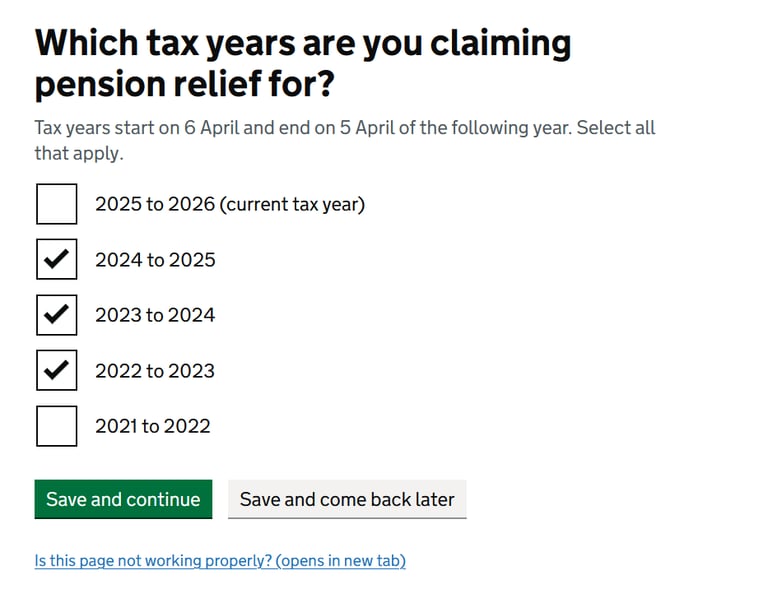

Below are some of the screen shots from the Online tool to see some of the questions that come up.

How far back can I claim?

If you have been a higher rate tax payer for a few years, all is not lost. You can backdate pension contributions for up to the last 4 years. That means for the 2025/26 tax year, you can still claim for.

What happens after you claim?

Here is the good news; the extra tax relief you claim does not have to go into your pension. You have a few options for how you receive it – the choice is entirely yours. You could get it as:

A tax rebate (HMRC sends you money back)

A reduction in your tax bill

A change to your tax code

No matter how you decide to get this money back, it is yours to keep. Now that is a win.

How does Workplace pension tax relief work?

There are 3 ways in which Workplace Pension Tax Relief Work

1. Salary Sacrifice: Your pension contributions are entirely paid by your employer and not subject to income tax. This arrangement means you have agreed to reduce part of your salary in exchange for pension contributions made by your employer. Without salary sacrifice, this part of your pension would have been subject to income tax and National Insurance deductions. Instead, your employer contributes this amount to your pension, free of these taxes. If you are paying pension contributions using salary sacrifice there is nothing for you to claim back from HMRC.

2. Net pay: Here your pension contributions are taken from your salary after National Insurance is deducted but before income tax is deducted. This means you only pay National Insurance on the contributions and no income tax needs to be claimed back from HMRC.

3. Relief at Source: Here your employer deducts your pension contribution after tax and National Insurance and if you are a higher rate or additional rate tax paper you will need to take steps to claim back the extra pension tax relief from HMRC. Here your pension provider will automatically claim basic tax relief on your behalf.

Don’t lose out. Claim It.

Claiming back the additional pension tax relief is an often missed but powerful opportunity to pay less tax and grow your pension.

Whether you are owed £300 or £5,000 don’t lose out by not claiming back what is yours.

If you have never completed a self-assessment tax return or just have questions we would love to help. Simply complete the contact form below and we will be in touch withing 24 hours, that is our promise.

Bookkeeping

Email:

Contact Us

support@rhodiumaccounting.co.uk

© 2026. All rights reserved | Privacy Policy | Terms and Conditions

Monthly Management Reporting

Budgets & Forecasts

Cash flow Optimisation

Processes and Controls