Workplace Pensions Made Simple: How to Grow Your Retirement Pot.

Workplace pensions can feel complicated, but they do not need to be. This guide breaks down how they work, the tax advantages they offer, and the different types you might come across. By the end, you will know how to make the most of your pension.

PENSIONS

What is a workplace pension?

A workplace pension is simply a way of saving for retirement straight from your pay. Contributions are taken directly from your wages, and in most cases your employer adds money as well. If you qualify for automatic enrolment, your employer is legally required to contribute too.

Many workplace pension schemes also come with extra benefits, such as support for your partner or dependants if you die while you are still working.

Your employer must automatically enrol you into a workplace pension if you:

Are aged between 22 and State Pension age

Earn at least £10,000 a year

Work in the UK

The two main types of workplace pension

There are two broad types of workplace pension schemes:

Occupational pension schemes

Group personal pensions or stakeholder pensions

Let’s look at each in turn.

Occupational pension schemes

Occupational pensions are set up and run by employers for their staff. There are two main types.

Final salary and career average schemes

Final salary schemes are also known as defined benefit schemes. These are often seen as the gold standard of workplace pensions.

In a final salary scheme, your pension is linked to your pay while you are working. As your salary increases, your future pension usually increases too. Your retirement income is worked out using your salary and how long you have been a member of the scheme.

Some schemes use your salary at or near retirement. Others use a career average approach, where your pension is based on your average earnings over the whole time you worked for the employer.

The key point is that your pension does not depend on how investments perform. The income is promised in advance, which makes it far more predictable.

In most final salary schemes, you pay a fixed percentage of your wages and your employer pays the rest. Because of how valuable these schemes are, it is usually a very good idea to join one if your employer offers it. That said, they are becoming increasingly rare, especially in the private sector.

These schemes are trust-based and the employer carries the investment risk. They typically offer:

A guaranteed income for life

Inflation-linked increases

Pensions for dependants after death

If a private sector employer fails, the Pension Protection Fund may step in to provide compensation.

Final salary and career average schemes are now mainly found in the public sector.

Money purchase schemes

Money purchase schemes are also called defined contribution schemes.

With these, there is no promised income. Instead, the money you and your employer pay in is invested, and the size of your pension depends on:

How much is paid in

How well the investments perform

You usually contribute a percentage of your wages, and your employer may also contribute, especially if you are automatically enrolled.

If your employer contributes, it is often well worth joining. If they do not, or if you are not eligible for automatic enrolment yet, it is sensible to compare the scheme with personal pensions available elsewhere.

Extra benefits of occupational schemes

Occupational pension schemes often come with added protection, such as:

Life cover that pays a lump sum or pension to your dependants if you die while employed

An ill-health pension if you have to retire early

Ongoing pensions for your spouse, civil partner, or other dependants

Group personal pensions and stakeholder pensions

Group personal pensions, often called GPPs, are workplace pensions set up through a pension provider rather than run directly by the employer.

They are always defined contribution schemes.

Your employer chooses the provider, but you have an individual contract with that provider. Contributions are deducted from your pay, invested, and build up into a pension pot that you later use to fund retirement.

The main difference compared with arranging your own personal pension is control. In a workplace scheme, the provider usually chooses the default investments for you. With a personal pension you arrange yourself, you often have more say over how your money is invested.

Your employer may contribute to a group personal or stakeholder pension, but they do not have to unless automatic enrolment rules apply. If there is no employer contribution, it is worth comparing costs and features with other pensions on the market.

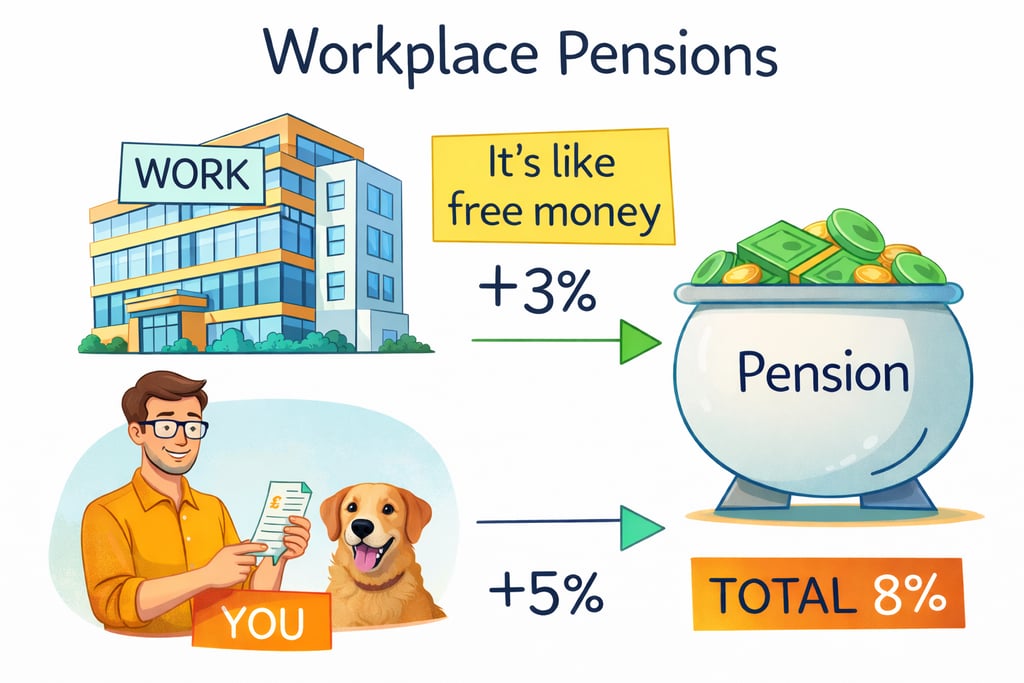

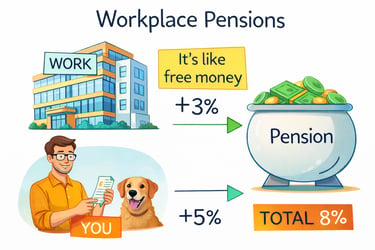

Once you are enrolled, you will save a small percentage of your salary. The government adds tax relief, and your employer will usually contribute at least 3 percent, and sometimes more.

Although pension contributions reduce your take-home pay, they can increase your entitlement to means-tested benefits and reduce student loan repayments.

Key differences between occupational and group pensions

The main differences can be summed up as follows:

Structure and management

Occupational schemes are run by trustees acting in members’ interests. Group pensions are contracts between you and the provider.Risk

Occupational schemes can be defined benefit or defined contribution. Group pensions are almost always defined contribution, so the investment risk sits with you.What happens when you leave

Occupational pensions can often stay in place when you leave. Group personal pensions usually separate from the employer arrangement.Control

Occupational schemes often use professionally managed funds. Group pensions are managed directly by the provider.

Both are workplace pensions and both can include employer contributions, but occupational schemes are usually more employer-led.

Taking money from your pension

You normally choose when to access your pension, usually from age 55, rising to 57 from April 2028.

You can usually take up to 25 percent as a tax-free lump sum. The rest is taxable.

You can take your pension in several ways:

As cash

By buying an annuity for guaranteed income

Using drawdown to take money as needed

As smaller lump sums over time

What is the best pension for you?

There is rarely a single best pension for everyone. The State Pension alone is unlikely to be enough for most people, so saving into another pension is usually sensible.

Start by thinking about what you want your retirement to look like. Many women reach retirement with smaller pension pots than men, known as the gender pension gap.

If you have several pension pots, consolidating them may reduce fees and make things easier to manage.

If you have a workplace pension, always check whether you are making the most of employer contributions. That is often free money you do not want to miss. Remember, pension values can go down as well as up.

What happens when you change jobs?

When you change jobs, you usually have a few options:

Leave your pension where it is

Transfer it to a new occupational scheme

Transfer it to a personal pension

This can be a difficult decision, and professional financial advice is often worthwhile.

If you were automatically enrolled, special rules apply when you leave employment. You can find more information on the DWP website.

Finally, always keep your pension providers updated if you change address. Lost pensions are surprisingly common and can cause real headaches later.

And you want to grow your pension quickly, why not get our tax guide that will show you how save tax and boost your pension post.

Blog content is for information purposes only and over time may become outdated as the tax landscape is constantly changing, although we do strive to keep it current and up to date. It is written to help you understand your taxes and is not to be relied upon as professional accounting, tax and legal advice.

Bookkeeping

Email:

Contact Us

support@rhodiumaccounting.co.uk

© 2026. All rights reserved | Privacy Policy | Terms and Conditions

Monthly Management Reporting

Budgets & Forecasts

Cash flow Optimisation

Processes and Controls